Get latest insights on payments, customer behavior and intelligence to improve your product.

How Biometrics is Shaping the Future of KYC and Payments

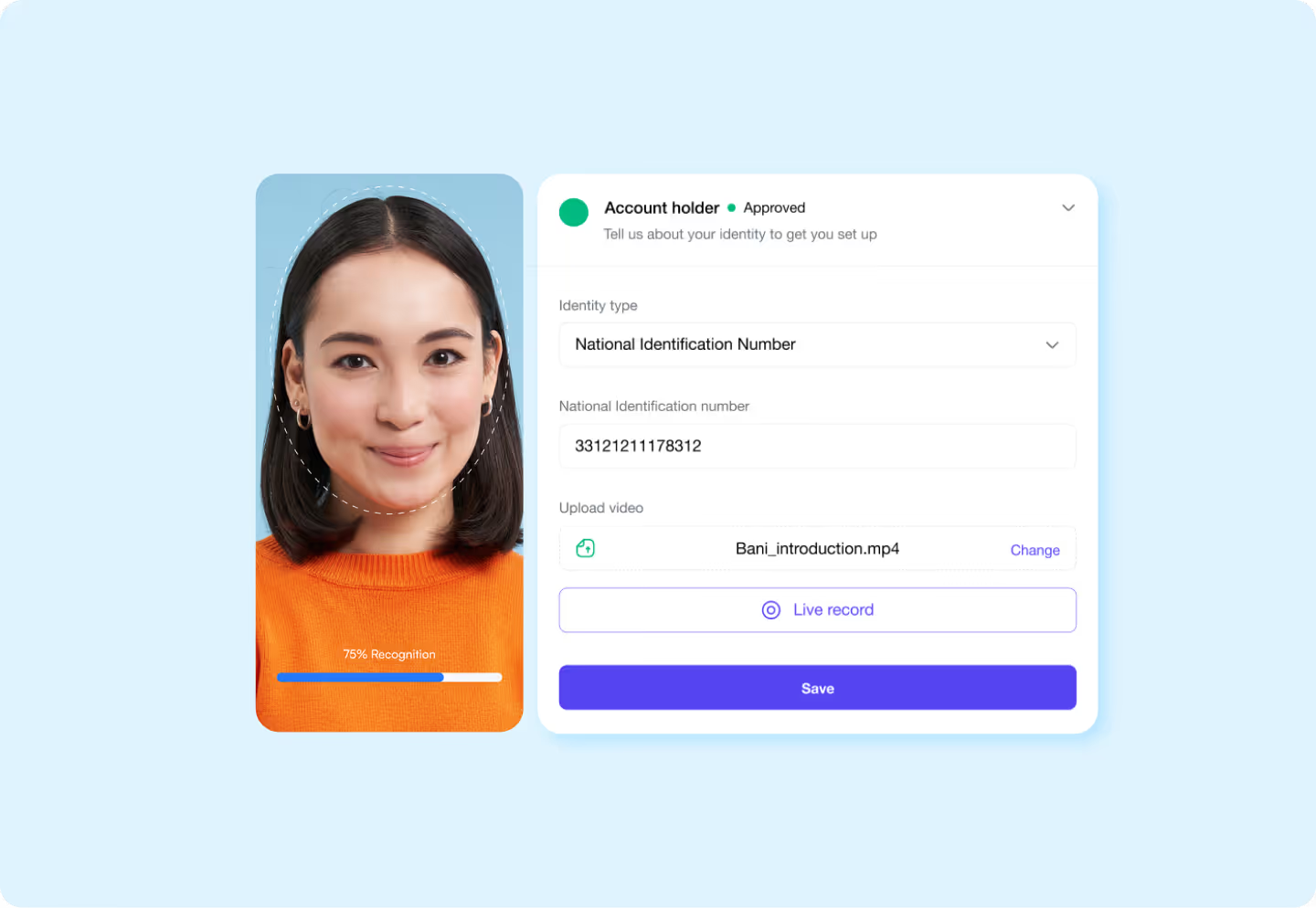

Neokred's digital KYC solution represents a significant leap forward in the way businesses approach identity verification. By harnessing the power of AI, and seamless integration, Neokred not only simplifies the KYC process but also enhances security and compliance.

The Evolution of KYC

KYC is a fundamental regulatory requirement aimed at preventing money laundering, fraud, and identity theft. Historically, KYC involved manual verification processes that required customers to submit physical documents, leading to delays and potential errors. The advent of digital KYC has transformed this space, enabling faster, more accurate, and seamless verification processes.

Neokred's Vision and Approach

Neokred is at the forefront of this digital transformation, offering cutting-edge solutions that simplify and streamline KYC procedures. Their approach is rooted in leveraging advanced technologies such as artificial intelligence (AI), machine learning (ML), and blockchain to create a secure, efficient, and user-friendly KYC process.

“In a world older and more complete than ours they move finished and complete, gifted with extensions of the senses we have lost or never attained, living by voices we shall never hear.”

Rohith Reji, CEO

Key Features of Neokred's Digital KYC Solution

- AI-Driven Verification

Neokred uses sophisticated AI algorithms to verify customer identities in real-time. By analyzing patterns and detecting anomalies, AI ensures that only genuine documents are accepted, significantly reducing the risk of fraud. - Seamless User Experience

The platform is designed with the end-user in mind, offering an intuitive interface that guides customers through the verification process effortlessly. Users can upload documents, capture selfies, and complete verification steps from the comfort of their homes. - Blockchain Security

Blockchain technology enhances the security of KYC data by creating an immutable ledger that is resistant to tampering. This ensures that customer data is protected and can be audited with transparency.

Success Stories

Several businesses have already reaped the benefits of Neokred's innovative KYC solution. For instance, fintech startups have been able to onboard new users within minutes, while traditional banks have significantly reduced their KYC processing times and costs. The positive impact on customer satisfaction and operational efficiency has been profound, demonstrating the transformative power of Neokred's technology.

The Future of KYC with Neokred

As digital transformation continues to reshape the financial industry, Neokred is poised to lead the charge in KYC innovation. The company is continually refining its technologies, exploring new applications for AI and blockchain, and expanding its global footprint. With a commitment to excellence and a vision for a secure, efficient, and customer-centric KYC process, Neokred is setting new standards in the industry.

Conclusion

Neokred's digital KYC solution represents a significant leap forward in the way businesses approach identity verification. By harnessing the power of AI, blockchain, and seamless integration, Neokred not only simplifies the KYC process but also enhances security and compliance. For businesses looking to stay ahead in a competitive market, embracing Neokred's innovation could be the key to unlocking greater efficiency, cost savings, and customer satisfaction.

GDPR vs DPDPA: What Indian Businesses Need to Know

GDPR vs DPDPA: What Indian Businesses Need to Know

Introduction

With the enforcement of the Digital Personal Data Protection Act (DPDPA) in India, businesses are facing a major shift in how they handle user data. While many are already familiar with the General Data Protection Regulation (GDPR) from the European Union, the Indian DPDPA brings a localized set of expectations that require careful alignment.

If your business operates online, handles user data, or targets customers in India, understanding the similarities and differences between GDPR and DPDPA is crucial to avoid non-compliance penalties and maintain user trust.

What Is GDPR and What Is DPDPA?

GDPR (General Data Protection Regulation) is a comprehensive data privacy regulation that governs the use of personal data of EU citizens. Enforced since 2018, it applies to any organisation inside or outside Europe that processes EU user data.

DPDPA (Digital Personal Data Protection Act, 2023) is India’s data protection law designed to address the digital privacy needs of Indian citizens. While inspired by GDPR, it focuses on Indian legal, social, and operational contexts.

Key Similarities

Both regulations are built on similar privacy principles such as lawful and fair data processing, data minimization, purpose limitation, and user consent. They also emphasize the importance of transparency, giving users access to their data, and ensuring organisations implement strong data security measures.

Important Differences Between GDPR and DPDPA

Despite similarities, there are critical differences businesses must understand:

- Scope and Applicability: GDPR applies globally to any entity handling EU citizen data, while DPDPA primarily applies to entities processing digital personal data of Indian citizens.

- Consent: Both require clear and informed consent, but DPDPA introduces the concept of “deemed consent” allowing processing in certain legitimate contexts without explicit permission, such as for employment or public interest.

- Age of Consent: GDPR sets the age of consent at 16 (with member states allowed to lower it to 13), whereas DPDPA fixes it at 18 across the board.

- Regulatory Authority: GDPR is enforced by individual Data Protection Authorities (DPAs) in each EU country. DPDPA will be enforced centrally by the Data Protection Board of India.

- Cross-Border Transfers: GDPR permits data transfers to countries with “adequate” privacy protections. DPDPA allows transfers to countries notified by the Indian government a more discretionary mechanism.

- Penalties: GDPR can fine up to €20 million or 4% of global turnover. DPDPA fines can go up to ₹250 crore, making it one of the strictest regimes in the APAC region.

- Data Subject Rights: GDPR grants broad rights including data portability and objection to processing. DPDPA offers rights like access, correction, erasure, and grievance redressal with some differences in implementation detail.

Why GDPR-Compliant Doesn’t Mean DPDPA-Compliant

Many businesses assume that GDPR compliance gives them automatic coverage under DPDPA. But DPDPA’s specific provisions like deemed consent, age requirements, and regional enforcement require a separate layer of localization.

Compliance with GDPR is a strong foundation, but not a full solution for Indian legal obligations.

How Blutic Helps You Navigate Both

Blutic is built to handle both GDPR and DPDPA compliance through a unified, region-aware platform. It helps businesses:

- Show location-based cookie consent banners

- Categorize cookies clearly with opt-in controls

- Record and store user preferences with timestamps

- Offer granular consent management for specific data purposes

- Integrate with tools like Google Tag Manager, Shopify, and WordPress

- Maintain consent logs for audit readiness

Whether you're an Indian business expanding to Europe or a global company entering India, Blutic ensures you're compliant, user-friendly, and future-proof.

India’s DPDPA reflects a maturing digital landscape, demanding accountability from businesses handling personal data. While it borrows foundational elements from GDPR, it introduces its own framework and enforcement style. Understanding these differences and acting early is the key to risk-free, trust-centric operations.

Blutic helps Indian businesses confidently navigate this evolving space by simplifying compliance without compromising user experience.

How Fintechs Can Reduce KYC Onboarding Drop-Off Caused by Form Fatigue

Why KYC Onboarding Still Struggles to Convert

In fintech onboarding, intent is rarely the issue. Users begin the journey willing to complete identity verification, yet a significant number never reach the end. Industry-wide, KYC and identity verification stages consistently see the highest abandonment especially when users are required to manually enter the same information multiple times across forms and document uploads. User patience hasn’t decreased. Expectations have increased.

The Cost of Form Fatigue in Fintech Onboarding

Repetitive onboarding flows introduce friction at the most sensitive stage of the user journey.

This typically shows up as:

- Long forms asking for identity and address details

- Document uploads that repeat already-entered information

- Multiple steps validating the same data

Each repetition adds effort. Each added step increases the likelihood of drop-off.

For businesses, this friction results in:

- Higher acquisition costs with lower activation rates

- Delayed customer onboarding

- Increased operational effort to follow up on incomplete applications

Form fatigue affects both conversion and efficiency.

Why This Problem Exists Across the Industry

Many onboarding systems were designed around verification completeness, not user effort minimisation.

As a result:

- Data capture and verification operate as separate stages

- Document uploads don’t meaningfully reduce form length

- Users are asked to provide the same information in different formats

When verification workflows are layered on top of forms instead of integrated into them, redundancy becomes visible—and frustrating.

What Efficient Onboarding Looks Like

Effective onboarding follows a simple principle:

Do not ask users to manually enter information that already exists in a verifiable form.

Instead:

- Verified data is reused within the onboarding flow

- Forms are shortened wherever possible

- Users confirm details rather than re-enter them

This keeps onboarding focused on validation, not repetition.

How ProfileX Supports This Approach

ProfileX, built by Neokred, supports onboarding flows where verified data is used to reduce unnecessary manual input.

ProfileX enables:

- Real-time verification of identity and address

- Support for both individual (KYC) and business (KYB) onboarding

- Validation of company registrations, tax IDs, licenses, and regulatory documents

The emphasis is on reducing redundant user effort while maintaining structured verification processes.

Automation Without Disrupting the User Journey

ProfileX supports automated KYC and KYB processes through configurable workflows that reduce manual intervention.

This helps:

- Maintain onboarding continuity

- Limit repeated user actions

- Keep the experience consistent across channels

Automation is applied to simplify the flow not to add complexity.

Fraud and Risk Signals During Onboarding

Onboarding is also a critical point for early risk detection.

ProfileX includes fraud and risk signaling using device intelligence, which:

- Analyses device behaviour during user interaction

- Identifies anomalies such as emulators, bots, or tampered devices

- Detects multiple accounts associated with the same device

These signals integrate into existing risk workflows and operate without interrupting genuine users.

Reducing Drop-Off Starts with Removing Repetition

Onboarding failures are rarely caused by lack of intent. They are more often caused by users being asked to repeat themselves.

By shortening forms, reusing verified data, and integrating verification directly into the flow, fintechs can reduce onboarding drop-offs without weakening compliance requirements.

What to Review in Your Onboarding Flow

If drop-offs consistently occur midway through onboarding, it’s usually a process signal.

Look for:

- Fields users have already provided elsewhere

- Uploads that don’t reduce manual effort

- Steps that validate the same data twice

That’s where friction starts and where improvement has the most impact.

Why Soundbox Devices Are Becoming Essential for Indian Merchants

Why Soundbox Devices Are Becoming Essential for Indian Merchants

India’s digital payments scale has exposed a gap that software alone cannot solve: real-time, unambiguous payment confirmation at the physical point of sale. Soundbox devices have emerged not as accessories, but as operational infrastructure for merchants handling high-frequency UPI transactions.

The Real Problem Soundboxes Solve: Payment Ambiguity at Scale

UPI works exceptionally well at the system level. The friction appears at the merchant execution layer.

In busy retail environments, merchants deal with:

- Simultaneous customers

- Multiple payment apps

- Network latency or delayed app notifications

- Human error during verification

The result is payment ambiguity situations where a customer claims success, but the merchant cannot instantly verify receipt. Soundbox devices eliminate this ambiguity by becoming a single source of truth at the counter.

Why Smartphone-Based Verification Fails in Real-World Conditions

Most merchant apps assume ideal conditions: one device, one transaction, one operator. Indian retail rarely works this way.

Operational limitations include:

- Shared phones across staff

- Battery drain and device downtime

- Notification overload

- App switching delays during peak hours

Soundboxes offload payment confirmation from smartphones to dedicated hardware, improving reliability without adding complexity.

Impact on Transaction Throughput and Queue Economics

In high-volume environments, even a 2–3 second delay per transaction compounds quickly.

Soundbox devices:

- Remove the need for manual checks

- Enable continuous transaction flow

- Reduce verbal confirmation loops with customers

For merchants processing hundreds of payments daily, this translates to:

- Shorter queues

- Higher throughput

- Better staff productivity

This operational efficiency directly affects revenue during peak periods.

Dispute Reduction and Operational Risk Control

UPI disputes are rarely about fraud they are about timing, visibility, and confirmation.

Soundbox devices help reduce:

- “Paid but not received” arguments

- Accidental double payments

- Missed transactions during rush hours

By announcing only confirmed credits, soundboxes introduce determinism into an otherwise probabilistic verification process.

Trust Signaling in Semi-Formal Retail Environments

In many Indian retail settings, trust is built in real time.

Audio confirmation:

- Signals transaction success to both parties

- Reduces dependency on visual proof

- Reinforces merchant legitimacy

This is particularly important in:

- Cash-heavy neighborhoods

- First-time digital payment users

- Tier-2 and tier-3 markets

Soundboxes quietly reinforce confidence in digital payments without requiring user education.

Integration with POS, QR, and Merchant Workflows

Modern soundbox deployments are no longer standalone.

They are increasingly:

- Linked to dynamic QR systems

- Integrated with POS terminals

- Synced with merchant dashboards and settlement systems

This integration ensures consistency across:

- Payment modes

- Transaction records

- End-of-day reconciliation

Soundboxes are becoming part of a cohesive merchant payments stack, not an isolated device.

Uptime, Connectivity, and Hardware Dependability

In payments, reliability is not a feature — it is a baseline requirement.

Soundbox devices are designed for:

- Continuous power availability

- Low-bandwidth connectivity

- Always-on operation

This makes them more dependable than consumer smartphones in retail environments, especially during long operating hours.

Soundboxes as Enablers of Merchant Digitization

Beyond confirmation, soundbox adoption has second-order effects:

- Encourages full digital acceptance

- Reduces cash handling

- Creates cleaner transaction records

- Supports future credit and analytics use cases

For small merchants, soundboxes act as a gateway device into structured digital commerce.

Strategic Importance in India’s Payment Infrastructure

India’s payment growth is not constrained by consumer adoption it is constrained by merchant-side execution.

Soundbox devices solve a uniquely Indian problem:

- Extremely high UPI volume

- Highly fragmented merchant base

- Real-world retail constraints

This is why soundboxes have moved from optional add-ons to core infrastructure.

Soundbox devices are not about convenience. They are about clarity, speed, and operational certainty at the moment money changes hands.

For Indian merchants operating at scale, soundboxes are no longer a nice-to-have — they are becoming essential to running digital-first commerce reliably.

How POS Devices Power Digital Payments in India

How POS Devices Power Digital Payments in India

India’s digital payments story is often told through UPI apps and mobile wallets. But behind millions of everyday card and QR transactions is a quieter enabler, the Point of Sale (POS) device.

From kirana stores and fuel stations to large retail chains, POS devices form the physical backbone of India’s digital payments ecosystem. They bridge the gap between consumers, merchants, banks, and payment networks turning digital money into real-world transactions.

The Role of POS Devices in India’s Payments Infrastructure

A POS device is more than a card-swiping machine. It is the final execution layer of digital payments — the point where authentication, authorization, and settlement come together in seconds.

In India, POS devices typically support:

- Debit and credit card payments

- Contactless (NFC) transactions

- QR-based payments linked to UPI

- Integration with billing and inventory systems

This versatility makes POS devices essential across both formal retail and small merchant ecosystems.

Why POS Devices Still Matter in a UPI-First Market

UPI dominates peer-to-peer and app-based payments, but POS devices continue to play a critical role for three reasons:

1. Card Payments Remain Core to Retail

Large-ticket purchases, credit-based transactions, and international cards still rely on POS terminals. Retailers cannot operate at scale without card acceptance.

2. Offline Commerce Needs Dedicated Hardware

Unlike app-to-app payments, in-store commerce requires:

- Stable connectivity

- Secure payment processing

- Quick transaction confirmation

POS devices are purpose-built for this environment.

3. Customer Trust at Checkout

A physical POS terminal signals legitimacy. For many customers, especially outside metros, POS acceptance increases confidence in the merchant and the transaction.

How POS Devices Enable Digital Payments End-to-End

Every POS transaction follows a structured flow:

- Payment initiation: card tap, swipe, insert, or QR scan

- Authentication: PIN, contactless limits, or UPI approval

- Authorization: communication with bank and payment network

- Transaction confirmation: approval or decline in real time

- Settlement: funds credited to the merchant

This entire process typically completes in a few seconds even in high-volume retail settings.

POS Devices and Financial Inclusion in India

POS expansion has played a quiet but powerful role in bringing small merchants into the digital economy.

- Enables acceptance of non-cash payments

- Reduces dependency on physical cash handling

- Creates transaction records useful for credit access

- Supports formalization of small businesses

Government-led initiatives and banking partnerships have accelerated POS adoption in tier-2, tier-3, and rural markets.

Security and Compliance at the Point of Sale

POS devices operate at a sensitive intersection of payments, personal data, and financial information.

Modern POS systems are designed to:

- Encrypt transaction data end-to-end

- Comply with card network security standards

- Support auditability and traceability

- Minimize exposure of customer information

As India strengthens its data protection and digital payment regulations, POS devices are evolving to meet higher standards of security and accountability.

The Evolution of POS in India

Today’s POS devices look very different from early card terminals.

New-generation systems now offer:

- Touchscreen interfaces

- Wireless and mobile connectivity

- Integration with billing, GST, and inventory

- Support for soundbox and QR confirmations

- Analytics and reporting for merchants

These advancements are turning POS terminals into business enablement tools, not just payment machines.

What’s Next for POS Devices in India?

As digital payments continue to grow, POS devices will increasingly focus on:

- Faster checkout experiences

- Smarter risk and fraud controls

- Deeper integration with merchant software

- Support for omnichannel commerce

Rather than being replaced by mobile apps, POS devices are becoming more intelligent adapting to India’s diverse retail and merchant landscape.

Digital payments in India are powered by apps, networks, and policies but they come to life at the counter.

POS devices remain a foundational part of this ecosystem, enabling trust, speed, and accessibility in everyday transactions. As commerce becomes more digital, the importance of reliable, well-designed POS systems will only continue to grow.

DPDP Compliance Timeline 2025–2027: What Goes Live and When

DPDP Compliance Timeline 2025–2027: What Goes Live and When

With the Digital Personal Data Protection Act, 2023 (DPDP Act) and the accompanying Digital Personal Data Protection Rules, 2025 now notified, Indian businesses must align their data practices to a clear schedule of compliance. The phased rollout provides a transition window, but the deadlines are firm, and non‑compliance carries serious risk. This blog breaks down what happens when, helping you stay ahead of each compliance milestone.

Why the Timeline Matters

The DPDP framework uses a staged implementation model: certain rules are in effect immediately; others take effect after 12 months, and the full regime becomes active about 18 months out. Understanding this structure helps you prioritize efforts, avoid last‑minute rushes, and ensure you meet each layer of obligations whether you're managing cookies, consent logs, or data retention.

Key Milestones You Should Know

Phase 1 – Immediate (November 13 2025)

On the date of Gazette notification, critical provisions come into force. These include:

- Rules 1, 2 and 17‑21 of the DPDP Rules (definitions, Board establishment, procedure) Bar and Bench - Indian Legal news+1

- Institutional frameworks such as the Data Protection Board of India being set up

- Basic obligations such as notice to Data Principals, initial definitions, and rule‑making authority

Phase 2 – After One Year (by November 13 2026)

This tranche triggers more operational obligations:

- Rule 4 (Registration and obligations of Consent Managers) takes effect.

- More extensive structures for consent manager frameworks, obligations of intermediaries

- Businesses must ensure platforms or interfaces for consent management are operational, and registration process begun

Phase 3 – After 18 Months (by May 13 2027)

The full backbone of the DPDP regime becomes active:

- Rules 3, 5 to 16, 22 and 23 (covering notice by fiduciaries, processing of personal data of children, cross‑border data transfer, rights of data principals, audit obligations of significant data fiduciaries) Bar and Bench - Indian Legal news+2Lakshmi Sri+2

- Data fiduciary obligations including consent capture, detailed logs, erasure rules, security safeguards

- The clock is now ticking for full compliance not just the initial pieces

What Your Business Should Be Doing at Each Stage

Immediately:

- Review and update your privacy notices, cookie banners, consent flows to reflect notice requirements.

- Set up logging and monitoring frameworks, plan for data breaches.

- Map out your data flows, categories of cookies, and identify which data relies on user consent.

Within 12 Months:

- Implement or integrate a consent management platform (such as Blutic) to support consent capture, withdrawal, and audit logs.

- Ensure registration or readiness for Consent Manager obligations if you serve as or rely on such services.

- Confirm vendor agreements and processor contracts include DPDP‑compliant terms.

By 18 Months (May 2027):

- Complete full rollout of all obligations: language‑specific notices, consent for children under 18, the erasure process, cross‑border transfer protocols, retention and logs for one year or more.

- Conduct internal audits, DPIAs for significant data fiduciaries, ensure board‑level oversight of data privacy.

- Prepare for enforcement and audit from the Data Protection Board.

A phased timeline gives businesses breathing room but only if they act now. Early preparation translates into stronger compliance, better user trust, and fewer surprises. With each phase comes more responsibility, and the full regime of the DPDP Act is just around the corner. Don’t wait until the final phase to begin start aligning today.

By leveraging tools like Blutic, businesses can implement necessary consent management and data‑privacy mechanisms in time for each milestone.

Unified Fraud Intelligence: Why Fragmented Fraud Systems Are Failing in 2026

Fraud in 2026 is faster, smarter, and more coordinated—yet most businesses still rely on fragmented detection systems. This disconnect creates blind spots, delays, and friction. Unified fraud intelligence solves this by bringing together device, behavior, and transaction signals into a single, real-time decision layer.

Unified Fraud Intelligence: Why Fragmented Fraud Systems Are Failing in 2026

Fraud has evolved. But most fraud detection systems haven’t.

Today’s fraud is:

- AI-driven

- Coordinated across networks

- Designed to bypass traditional checks

Yet businesses still rely on fragmented tools separate systems for KYC, device checks, transaction monitoring, and behaviour analysis.

The result?

Blind spots, delays, and poor user experience.

The Problem: Fragmented Fraud Stacks

Most businesses operate with:

- Multiple vendors across onboarding and transactions

- Disconnected fraud signals

- Delayed decision-making systems

This leads to:

- Broken customer journeys

- High false positives

- Increased operational costs

Fraud isn’t isolated anymore. Your detection systems shouldn’t be either.

Why Traditional Fraud Detection Fails

1. Signals Are Not Connected

Device, behavior, and transaction signals are analyzed separately.

Fraud, however, operates across all three.

2. Detection Happens Too Late

By the time fraud is flagged, the damage is already done.

3. Customer Experience Suffers

False declines increase friction and reduce conversions.

What Unified Fraud Intelligence Means

Unified fraud intelligence brings together:

- Device intelligence

- Behavioral biometrics

- Transaction signals

- Digital fingerprinting

Into a single decision layer. Instead of trusting one signal, it correlates hundreds.

How ProfileX Solves This

ProfileX unifies 200+ real-time risk signals across:

- Onboarding

- Authentication

- In-app monitoring

- Transactions

This enables:

- Faster fraud detection

- Reduced false positives

- Seamless user journeys

Fraud is no longer a single event. It’s a pattern. And patterns can only be detected when signals are connected.

Why Soundboxes Are Becoming Essential for Modern Merchants

Soundboxes enable instant voice-based payment confirmations, helping merchants eliminate manual checks, reduce fraud, and improve checkout speed. They are becoming a key part of modern payment infrastructure.

Why Soundboxes Are Becoming Essential for Modern Merchants

Digital payments have scaled rapidly. But the way merchants confirm those payments hasn’t always evolved at the same pace.

Even today, many transactions still depend on:

- Checking mobile screens

- Waiting for SMS alerts

- Verifying customer confirmations

This creates friction especially during peak hours.

The Need for Instant Confirmation

As transaction volumes increase, merchants need more than just payment acceptance. They need clarity instantly.

Every delay:

- Slows down queues

- Interrupts workflow

- Introduces uncertainty

What Changes with Soundboxes

Soundboxes remove this friction completely.

The moment a payment is successful, it is announced out loud.

No checking.

No waiting.

No doubt.

Key Benefits for Merchants

1. Faster Checkout Flow

Serve more customers without interruptions.

2. Reduced Fraud Risk

Eliminates reliance on screenshots or manual confirmation.

3. Improved Efficiency

Handle higher transaction volumes with ease.

4. Better Customer Trust

Clear audio confirmation builds confidence.

5. Works Across Payment Modes

Supports UPI, QR payments, wallets, and more.

Designed for Real-World Environments

Soundboxes are especially useful in:

- Retail stores

- Food outlets

- Petrol pumps

- Pharmacies

- Small and mid-sized businesses

Anywhere speed and clarity are critical.

From Device to Infrastructure

Soundboxes are evolving beyond standalone devices. They are becoming part of a broader system with:

- Cloud connectivity

- Analytics and reporting

- Remote updates

- Scalable deployment

They are no longer just tools. They are infrastructure.

Where Neokred’s Uniq Devices Stand Out

Neokred’s Uniq Soundboxes are built with a full-stack approach.

They combine:

- Instant voice confirmations

- Reliable performance under load

- Multi-language support

- Secure communication and device management

This enables businesses to deploy and scale without operational complexity.

The difference between a completed payment and a trusted one is clarity. And clarity should never take time.

How Soundboxes Work: The Technology Behind Instant Payment Alerts

Soundboxes are voice-enabled devices that announce digital payments in real time. Powered by cloud infrastructure, IoT connectivity, and intelligent audio systems, they eliminate manual verification and make merchant payments faster and more reliable.

How Soundboxes Work: The Technology Behind Instant Payment Alerts

Digital payments today are expected to be seamless. Customers scan, pay, and move on often in seconds. But for merchants, confirming those payments has traditionally required an extra step.

Checking a screen, Waiting for a message, Verifying before m oving ahead. That extra step, repeated across dozens of transactions, creates friction.

This is where Soundboxes come in. They remove the need to check. Instead, the system confirms the transaction instantly, audibly, and reliably.

What is a Soundbox?

A Soundbox is a voice-enabled payment device that announces successful transactions in real time.

Instead of relying on phones or apps, merchants hear:

“₹250 received”

This turns payment confirmation into something automatic not manual.

How Soundboxes Work (Step-by-Step)

The experience is simple. The system behind it is not.

1. Payment is Initiated

The customer scans a QR code linked to the merchant’s account and completes the transaction via UPI or other digital payment methods.

2. Transaction is Processed

The payment is routed through the bank or payment service provider and completed in real time.

3. Backend Notification is Triggered

A confirmation is sent to the merchant backend or aggregator system.

4. Soundbox Receives Real-Time Alert

The device receives the alert via:

- SIM-based connectivity

- Wi-Fi

- Or dual-mode communication

Using low-latency protocols like MQTT or WebSocket, the notification reaches the device instantly.

5. Voice Confirmation is Played

The Soundbox processes the data and announces the transaction using:

- Text-to-Speech (TTS)

- Or pre-recorded audio

6. Optional Visual Indicators

Some devices also display transaction details, connectivity status, or battery levels.

7. Offline Handling

In case of network issues, the system can cache alerts and play them once connectivity is restored.

The Technology Behind Soundboxes

What sounds like a simple voice alert is powered by a full-stack system:

Hardware Layer

- Microcontroller for processing

- High-volume speaker system

- SIM/Wi-Fi connectivity

- Rechargeable battery with long backup

Firmware Layer

- Real-time operating system (RTOS)

- Secure boot and device integrity checks

- Audio management and playback control

Cloud & Communication Layer

- Real-time transaction routing

- Secure device authentication

- Instant push notifications

- Analytics and logging

Audio Engine

- Multi-language voice support

- Dynamic audio generation

- Brand-customizable prompts

Why Soundboxes Matter for Merchants

Soundboxes solve a very real operational challenge:

- No need to check screens

- Faster checkout flow

- Reduced manual verification

- More confidence in every transaction

For high-volume environments, this directly improves efficiency.

Where Neokred Fits In

Neokred offers a full-stack Soundbox solution covering hardware, firmware, cloud infrastructure, and real-time communication.

This includes:

- Instant payment detection

- Voice-based confirmations

- Multi-language audio support

- Secure, encrypted communication

- Remote device management and OTA updates

The focus is not just on enabling alerts but on building a system that is reliable, scalable, and ready for real-world merchant environments.

.jpeg)

How AI is Changing the Way India’s Offline Merchants Accept Payments

AI is transforming offline payments by removing the need for manual verification. With real-time detection, instant confirmations, and intelligent monitoring, transactions are becoming faster, more reliable, and seamless for merchants | Neokred

How AI is Changing the Way India’s Offline Merchants Accept Payments

For years, offline payments in India followed a simple rhythm.

A customer paid.

The merchant checked.

The transaction was confirmed.

It worked but it depended heavily on manual verification.

Every transaction required attention.

Every confirmation needed a check.

And during peak hours, even a few seconds of delay could slow everything down.

Today, that model is quietly changing. Not because payments themselves are new, but because the systems behind them are becoming more intelligent. At the centre of this shift is AI.

AI is Removing the Need to Verify

One of the most visible changes is how payments are confirmed.

Earlier, merchants relied on:

- Customer screens

- SMS alerts

- App refreshes

Now, AI-enabled systems detect transactions in real time by continuously monitoring payment signals across networks.

The result:

- Instant payment recognition

- Voice confirmations without delay

- No need for manual cross-checking

The system doesn’t wait to be checked. It knows when a payment is complete.

AI is Identifying What Doesn’t Look Right

Offline payments have always had edge cases fake confirmations, delayed updates, or mismatched transactions.

AI addresses this by analysing multiple signals simultaneously:

- Transaction timing vs confirmation timing

- Device and network behaviour

- Payment pattern anomalies

Instead of relying on instinct, the system flags inconsistencies in real time. Most of this happens in the background but it changes how confidently merchants operate.

AI is Optimising Speed During Peak Load

As transaction volumes increase, maintaining performance becomes critical.

AI-driven POS systems help by:

- Dynamically managing transaction flow

- Reducing latency during high traffic

- Maintaining system stability under load

So whether it’s a steady stream or a sudden rush, the system keeps pace without slowing the merchant down.

AI is Turning Transactions into Intelligence

Beyond individual payments, AI helps systems learn over time.

Patterns begin to emerge:

- When peak hours occur

- How transaction volumes fluctuate

- What “normal” looks like for a business

This turns a POS system into more than a transaction tool it becomes a layer of operational awareness.

What This Means for Merchants

AI isn’t adding complexity.

It’s removing it.

- Fewer manual checks

- Faster movement during rush hours

- Reduced dependency on guesswork

- More confidence in every transaction

What changes is not just speed but how seamless the entire experience becomes.

Where Neokred’s Uniq Devices Fit In

This shift toward intelligent payments isn’t theoretical, it’s already being built into the devices merchants use every day.

Neokred’s Uniq range of POS and Soundbox devices is designed to bring together:

- Real-time payment detection for instant confirmations

- Voice-based alerts that remove the need to check screens

- Reliable performance under high transaction volumes

- Seamless integration with UPI and digital payment flows

The focus isn’t just on enabling payments. It’s on ensuring that every transaction is:

- Clear

- Immediate

- Dependable

So merchants can focus on serving customers not verifying transactions.

The Shift is Subtle, But Foundational

There are no new steps to learn, no added effort. The difference lies in what no longer needs to be done.

No checking, No waiting, No second-guessing.

Offline payments are no longer just about completing transactions.

They are becoming systems that:

- Validate

- Adapt

- Learn

All in real time. The biggest impact of AI in offline payments isn’t what merchants see. It’s what they no longer have to do.

What Is a UPI Soundbox and Why It’s Transforming Retail Payments in India

What Is a UPI Soundbox and Why It’s Transforming Retail Payments in India

What Is a UPI Soundbox?

A UPI Soundbox is a compact speaker device placed at a merchant’s counter. When a customer pays using UPI by scanning a QR code, the device announces the payment amount out loud for example:

“Received ₹250.”

This removes the need for merchants to check SMS messages or mobile apps manually.

The device is linked directly to the merchant’s UPI ID and receives real-time transaction confirmations.

How Does a UPI Soundbox Work?

The process is simple:

- The customer scans the merchant’s UPI QR code.

- The payment is completed via a UPI app.

- The transaction is processed through the UPI network.

- The soundbox receives confirmation.

- The device announces the amount instantly.

Most soundboxes use built-in SIM connectivity, so merchants do not need to depend on their personal phones for alerts.

Why UPI Soundboxes Were Introduced

As UPI adoption surged across India, merchants faced new challenges:

- Fake payment screenshots

- Delayed SMS confirmations

- Time wasted checking phones

- Disputes over whether payment was received

UPI Soundboxes were introduced to provide immediate, verified confirmation reducing friction at the counter.

Key Benefits for Retailers

Instant Verification

No need to check a mobile device repeatedly.

Fraud Reduction

Audio confirmation linked directly to the UPI network reduces screenshot fraud.

Faster Checkout

Transactions are confirmed in seconds, improving customer flow.

Hands-Free Convenience

Merchants can continue serving customers without interrupting work.

Why UPI Soundboxes Are Transforming Retail Payments

India’s retail sector includes millions of small merchants who are rapidly adopting digital payments.

UPI Soundboxes support this shift by:

- Increasing merchant confidence in digital transactions

- Encouraging customers to pay via UPI

- Reducing payment disputes

- Improving operational efficiency

For kirana stores, street vendors, pharmacies, and restaurants, the device simplifies digital acceptance.

The UPI Soundbox may look like a small device, but its impact on India’s retail ecosystem is significant.

By delivering instant voice confirmation, it has improved trust, speed, and transparency in digital transactions.

As retail payments continue to shift toward UPI and real-time digital acceptance, merchants increasingly need reliable, connected payment infrastructure that reduces friction at checkout.

For businesses looking to deploy secure, scalable UPI Soundbox solutions and modern payment devices, Neokred’s Soundbox infrastructure is designed to support real-time transaction confirmation, multi-language announcements, and seamless integration into today’s retail environments.

Digital payments are no longer optional and the right infrastructure makes all the difference.

The Evolution of POS Systems: From Card Swipes to Smart Retail Infrastructure

The Evolution of POS Systems: From Card Swipes to Smart Retail Infrastructure

What Is a POS System?

A POS (Point of Sale) system is the hardware and software used by businesses to process customer transactions.

Traditionally, POS systems were used only to:

- Swipe debit and credit cards

- Authorise transactions

- Print receipts

Today, POS systems have become multi-functional retail platforms that manage payments, data, and operations together.

Phase 1: The Era of Card Swipe Machines

In the early days of digital payments, POS machines were simple card terminals.

They allowed merchants to:

- Accept debit and credit cards

- Authorise transactions via bank networks

- Generate printed receipts

These devices were standalone and focused purely on card payments. They did not support analytics, inventory management, or multi-channel integration.

Phase 2: EMV, Contactless & Multi-Payment Acceptance

As payment technology evolved, POS systems began supporting:

- EMV chip-based cards

- Contactless tap payments

- NFC-enabled cards

- Mobile wallets

This shift improved security and speed while expanding customer payment choices. POS machines became more secure and compliant with global payment standards.

Phase 3: The Rise of UPI and QR-Based Payments

India’s digital payment revolution accelerated with UPI.

Modern POS systems began integrating:

- UPI QR acceptance

- Real-time transaction processing

- Instant payment confirmation

Retailers were no longer limited to card payments. POS infrastructure had to adapt to a multi-mode environment. This marked a major turning point in retail payments.

Phase 4: Smart POS and Connected Retail Infrastructure

Today’s POS systems are no longer just payment terminals.

They function as smart retail infrastructure by offering:

- Multi-payment acceptance (cards, UPI, wallets)

- Cloud-based reporting

- Inventory management integration

- GST-compliant billing

- Customer data insights

- Digital reconciliation

Modern POS devices are often Android-based, app-enabled, and connected to cloud dashboards. Retailers can now track sales in real time, manage stock, and analyse performance all from a single system.

Why POS Systems Had to Evolve

Several factors drove the transformation:

1. Growth of Digital Payments

India’s rapid adoption of cards, UPI, and wallets required flexible POS solutions.

2. Need for Faster Checkout

Retail environments demand speed. Integrated systems reduce friction and queue times.

3. Data-Driven Retail

Retailers now rely on sales analytics, demand forecasting, and digital reconciliation.

POS systems became a data engine, not just a payment tool.

4. Omnichannel Commerce

Businesses operate both online and offline. Modern POS systems help unify transactions across channels.

What Makes a POS System “Smart” Today?

A smart POS system typically includes:

- Multi-mode payment support

- Cloud connectivity

- App-based functionality

- Real-time reporting

- Secure transaction processing

- Integration with accounting tools

It serves as the central operational hub of a retail business.

The Future of POS Systems in India

POS infrastructure is expected to become even more intelligent.

Emerging trends include:

- AI-driven sales insights

- Integrated loyalty programs

- Contactless-first environments

- Embedded financing options

- Seamless UPI integration

As retail modernises, POS systems will continue to move from standalone devices to fully integrated digital ecosystems.

POS systems have evolved from simple card terminals to intelligent retail infrastructure that powers payments, reporting, and operational efficiency.

In today’s digital economy, businesses require POS machines that support multiple payment modes, real-time reconciliation, and connected retail operations.

Modern POS infrastructure must be secure, scalable, and adaptable to UPI-driven retail environments.

Neokred’s POS machines and integrated Soundbox solutions are built to support this next phase of smart retail enabling merchants to accept digital payments seamlessly while maintaining operational visibility and reliability.

As retail continues to digitise, choosing the right POS infrastructure becomes a strategic decision, not just a transactional one.

Consent Under the DPDP Act: What Businesses Must Build

Consent Under the DPDP Act: What Businesses Must Build

Why Consent Is Central to the DPDP Act

The DPDP Act makes lawful processing of personal data conditional on valid consent (in most business use cases).

Consent is no longer symbolic. It is enforceable and accountable.

The shift is clear: From collecting agreement to engineering proof.

What the DPDP Act Requires for Valid Consent

Consent must be:

- Free from coercion or dark patterns

- Specific to clearly defined purposes

- Informed through transparent notices

- Unambiguous through clear affirmative action

- Revocable as easily as given

- Verifiable through structured records

If any one of these elements is missing, consent may not meet compliance standards.

What Businesses Must Build to Comply

Understanding the law is not enough. Systems must support it. To meet DPDP consent requirements, businesses must implement:

Structured Consent Capture

Consent must be stored purpose-wise, not as a single “accepted” flag.

Purpose Mapping

Each processing activity must align with a declared purpose. Secondary use without fresh consent creates compliance risk.

Version Tracking

If consent language changes, the system must record which version each user agreed to.

Consent Lifecycle Management

Consent is dynamic. Systems must track:

- Given

- Updated

- Withdrawn

- Expired

Withdrawal Enforcement

Withdrawal must be easy and must automatically restrict further processing. If withdrawal does not propagate across systems, compliance gaps appear.

Audit-Ready Consent Logs

Businesses must be able to produce:

- Timestamp of consent

- Notice version

- Purpose mapping

- Current consent status

This must be exportable and regulator-ready.

Manual records or fragmented systems create operational risk.

Why Most Businesses Are Underprepared

Many organisations believe they are compliant because they:

- Have a cookie banner

- Store a timestamp

- Mention consent in privacy policy

But DPDP requires structured, enforceable consent infrastructure.

Common gaps include:

- No purpose-level tagging

- No real-time consent validation

- No automated withdrawal propagation

- No audit-ready consent exports

- No integration between frontend consent and backend processing

Consent that cannot be demonstrated is legally fragile.

Consent Is Now Infrastructure

The DPDP Act transforms consent into a technical function.

Legal defines requirements. Product designs the interface. Engineering must build enforceable systems.

Consent must now exist as:

- Structured data

- Processing rules

- Validation checkpoints

- Automated lifecycle logic

- Continuous monitoring

This is where many businesses struggle because consent was never built as infrastructure.

The Role of Consent Management Platforms

To meet DPDP standards at scale, businesses increasingly require dedicated consent management systems that:

- Capture purpose-specific consent

- Maintain version-controlled notices

- Enable easy withdrawal

- Track consent lifecycle events

- Generate audit-ready reports

- Integrate with backend systems

Without a structured consent management layer, organisations often rely on patchwork solutions across marketing tools, product databases, and CRM systems.

That fragmentation increases compliance risk.

Building DPDP-Ready Consent Architecture

A DPDP-aligned consent system should:

- Separate purposes clearly

- Ensure equal prominence of accept and reject options

- Provide user-accessible preference dashboards

- Store consent logs in structured, queryable formats

- Trigger automated updates when consent changes

- Support compliance reporting instantly

Purpose-built platforms such as Blutic are designed to support this transition transforming consent from a superficial banner into a backend compliance engine.

Blutic enables:

- Purpose-based consent capture

- Structured consent logging

- Real-time withdrawal workflows

- Version-controlled notices

- Audit-ready reporting aligned with DPDP expectations

Rather than retrofitting compliance into existing systems, businesses can integrate consent management as a foundational layer.

Consent under the DPDP Act is no longer a user interface element.

It is compliance infrastructure.

Businesses must build systems that:

- Capture consent clearly

- Map it to defined purposes

- Track lifecycle changes

- Enforce withdrawal automatically

- Generate audit-ready proof

Organisations that treat consent as documentation risk exposure. Those that engineer consent into their systems build resilience.

As DPDP enforcement matures in India, businesses that implement structured consent architecture through specialised platforms like Blutic position themselves for scalable, regulator-ready compliance without disrupting user experience.

In the DPDP era, consent is not collected. It is built.

What the DPDP Act Means for Digital Infrastructure in India

What the DPDP Act Means for Digital Infrastructure in India

India’s digital economy runs on applications, APIs, databases, payment flows, cookies, mobile apps, SaaS dashboards, and backend systems that continuously process personal data.

The DPDP Act shifts the responsibility of compliance from legal documentation to technical architecture.

The key question today is not: "Do we have a privacy policy?”

It is: “Can our systems technically enforce purpose limitation, consent validity, and audit traceability?”

This is why the DPDP Act directly impacts digital infrastructure in India.

A Quick Overview of the DPDP Act

The Digital Personal Data Protection Act, 2023 governs how personal data must be:

- Collected

- Processed

- Stored

- Protected

- Deleted

It introduces core obligations such as:

- Clear and informed consent

- Data minimisation

- Right to withdraw consent

- Accountability of data fiduciaries

- Significant financial penalties for violations

Every digital business that processes personal data must align its systems accordingly.

From Policy Compliance to System Compliance

Before DPDP, compliance often existed in documents:

- Privacy policies

- Terms and conditions

- Static cookie banners

- Manual audit files

After DPDP, compliance must be embedded into:

- Backend logic

- Database structures

- Consent storage mechanisms

- API workflows

- Access control systems

In other words, compliance must be enforced by code. If your infrastructure cannot technically prevent misuse of data beyond declared purposes, you may face regulatory exposure.

Purpose Limitation Is Now a Technical Requirement

One of the most important principles under DPDP is purpose limitation. Personal data can only be used for the specific purpose clearly communicated at the time of consent.

This has architectural implications.

Digital systems must now:

- Tag data with defined purposes

- Prevent reuse of data for unrelated objectives

- Maintain structured records of declared purposes

- Support new consent if purposes change

Without system-level controls, purpose limitation becomes impossible to enforce consistently.

Consent Must Be Verifiable: Not Just Collected

Under DPDP, consent must be:

- Free

- Specific

- Informed

- Unambiguous

- Revocable

But most importantly, it must be verifiable. This means digital infrastructure must support:

- Timestamped consent logs

- Version control of consent notices

- Purpose-linked consent records

- Real-time validation of consent status

- Easy withdrawal mechanisms

If a regulator or data principal questions processing activity, the organisation must be able to produce proof instantly. Consent cannot live in spreadsheets or static tables. It must be structured, searchable, and exportable.

Withdrawal of Consent Must Be as Easy as Giving It

The DPDP Act clearly states that withdrawal of consent must be as easy as giving it. From an infrastructure standpoint, this requires:

- User-accessible consent dashboards

- Automated revocation triggers

- Downstream system updates

- Real-time enforcement across integrated platforms

If withdrawal does not propagate across systems, compliance gaps emerge. Infrastructure must be interconnected enough to respect consent lifecycle events.

Data Retention and Deletion Are Infrastructure Problems

The Act also reinforces that personal data cannot be retained indefinitely without purpose.

This requires digital systems to implement:

- Defined retention policies

- Automated deletion triggers

- Archival logic

- Data lifecycle tracking

Manual deletion processes are no longer sufficient. Retention governance must be embedded into data architecture.

Audit Readiness Is Continuous, Not Occasional

Under DPDP, accountability is ongoing.

Digital infrastructure must support:

- Real-time logging

- Traceable data flows

- Access history records

- Exportable compliance reports

Waiting until an audit notice arrives is too late. Audit readiness must be built into the system by design.

Why This Is a Strategic Shift for India’s Digital Economy

India’s digital ecosystem is growing rapidly across fintech, SaaS, marketplaces, healthcare platforms, edtech, and government integrations.

The DPDP Act signals a maturation phase.

Digital infrastructure must evolve from:

Reactive compliance → Proactive compliance

Static documentation → Dynamic governance

Surface-level consent → Structured consent architecture

This shift increases trust, reduces regulatory risk, and creates more resilient digital systems.

Conclusion

The DPDP Act is not just a legal reform. It is an infrastructure reform. Digital systems in India must now embed:

- Purpose-based data processing

- Verifiable consent management

- Withdrawal enforcement

- Automated retention control

- Continuous audit readiness

Compliance is no longer a checkbox. It is a system capability.

For organisations looking to operationalise structured consent management aligned with DPDP requirements, purpose-built consent management platforms such as Blutic help transform consent from a front-end banner into a verifiable, audit-ready infrastructure layer.

The future of digital infrastructure in India will belong to systems that are compliant by design not compliant by exception.

When Financial Identity Breaks, Wealth Becomes Invisible

Weak or fragmented financial identity data can obscure true wealth, leading to misplaced assets, unclaimed funds, and challenges in accessing financial benefits.

When Financial Identity Breaks, Wealth Becomes Invisible

Unclaimed funds in India are often discussed in terms of money crores lying idle in banks, insurance companies, and government funds. But at a deeper level, these funds exist because financial identities break apart over time.

What starts as a valid, verified customer relationship slowly becomes unrecognisable as people change jobs, cities, names, contact details, and life circumstances. When systems fail to reconnect these identities, money turns into invisible wealth.

Financial Identity Is Not a Single Record

Most financial systems treat identity as a point-in-time event:

- KYC at account opening

- Nominee details at purchase

- Static records stored indefinitely

In reality, identity is dynamic. Over a lifetime, individuals accumulate multiple financial relationships that are never fully reconciled.

This gap explains why:

- Bank deposits become dormant

- Insurance policies go unclaimed

- PF and pension accounts are forgotten

- Dividends fail to reach shareholders

Siloed Systems Multiply Identity Gaps

Each financial institution operates its own data stack:

- Banks

- Insurance companies

- Employers

- Pension administrators

- Capital market intermediaries

Even though all are regulated by authorities such as the Reserve Bank of India and the Insurance Regulatory and Development Authority of India, identity data is not interoperable.

As a result:

- The same person exists as multiple records

- Updates in one system never propagate

- Ownership continuity silently erodes

When Time Breaks Identity

Unclaimed funds rarely arise overnight. They are the outcome of long time horizons.

Over 10–30 years, people experience:

- Migration and address changes

- Job switches and employer exits

- Name changes after marriage

- Loss of documentation

- Death without consolidated records

Legacy identity systems were not designed to survive decades of change.

Nominees Don’t Solve Discovery

Nominee frameworks exist but discovery remains weak:

- Nominees may be unaware of policies

- Families may not know where assets exist

- Documentation may be incomplete

Without discoverability, nomination alone cannot prevent funds from becoming unclaimed.

Invisible Wealth Is a Trust Problem

When families discover unclaimed funds late or never trust erodes:

- Individuals lose faith in institutions

- Institutions face operational and reputational burden

- Recovery becomes manual and emotionally costly

Unclaimed funds are therefore not just an operational issue they are a trust continuity failure.

The Infrastructure Shift Needed

Preventing invisible wealth requires:

- Persistent identity resolution

- Relationship mapping across time

- Secure, privacy-aware data reconciliation

- Recognition of individuals beyond onboarding

Identity must be treated as infrastructure, not paperwork.

Unclaimed Insurance Money in India

Policies with outdated identity information, unclaimed payouts, or forgotten beneficiaries often result in unclaimed insurance money, highlighting the need for accurate records and proactive follow-ups.

Unclaimed Insurance Money in India: How Forgotten Policies Leave Crores Unclaimed

Insurance is designed to provide financial protection at critical moments yet a surprising amount of insurance money in India remains unclaimed. These unclaimed amounts include life insurance maturity proceeds, survival benefits, and even death claims that were never settled because beneficiaries did not come forward or were unaware of the policy’s existence.

To protect policyholders and beneficiaries, Indian insurance regulations require insurers to identify, disclose, and safeguard unclaimed insurance money ensuring it remains fully claimable by rightful owners or legal heirs at any time.

What Is Unclaimed Insurance Money?

Unclaimed insurance money refers to policy proceeds that have become due but remain unpaid because the insurer could not successfully disburse them to the policyholder or nominee.

This typically includes:

- Life insurance maturity proceeds

- Survival benefits under endowment policies

- Death claims not claimed by nominees or legal heirs

- Refunds or residual balances under lapsed or discontinued policies

Unclaimed insurance money does not lapse or get forfeited it remains payable indefinitely.

Who Regulates Unclaimed Insurance Money in India?

All insurance companies in India operate under the oversight of the Insurance Regulatory and Development Authority of India (IRDAI).

IRDAI mandates insurers to:

- Periodically identify unclaimed and unpaid amounts

- Attempt to trace policyholders or nominees

- Disclose unclaimed amounts publicly

- Maintain accurate policy and nominee records

These requirements exist to ensure transparency and consumer protection.

Types of Insurance Money That Go Unclaimed

1. Unclaimed Life Insurance Maturity Proceeds

When a policy reaches maturity, the insurer is required to pay the maturity amount. If the policyholder:

- Has changed address or contact details

- Is unaware of the maturity

- Has multiple legacy policies

the proceeds may remain unpaid and become unclaimed.

2. Unclaimed Death Claims

Death claims often go unclaimed when:

- Nominees are unaware of the policy

- Nominee details are missing or outdated

- Legal heirs lack documentation

- Policies were purchased decades earlier

These are among the most sensitive and complex unclaimed insurance cases.

3. Unclaimed Survival Benefits

In policies with periodic payouts, survival benefits may remain unpaid if policyholders fail to respond to insurer communications or update bank details.

Why Do Insurance Policies Go Unclaimed?

Unlike bank accounts, insurance policies are often long-term and low-touch, making them easier to forget.

Common reasons include:

- Policyholders purchasing multiple policies over time

- Change in address, phone number, or email

- Lack of nominee awareness

- Death of the policyholder without consolidated records

- Poor documentation passed on to family members

In many cases, families discover policies only years later.

How Insurers Identify and Handle Unclaimed Amounts

As per IRDAI guidelines, insurers must:

- Categorize unpaid amounts based on duration

- Make reasonable efforts to contact policyholders or nominees

- Publish unclaimed amount details on their websites

- Maintain internal systems to track unpaid claims

These disclosures are intended to help beneficiaries discover forgotten policies.

How to Check for Unclaimed Insurance Money

Individuals or legal heirs can:

- Search insurer websites for unclaimed amount disclosures

- Contact insurance companies directly with basic identity details

- Review old documents, emails, or bank statements for premium payments

- Check policies issued under previous employers or group schemes

Unlike banking, insurance discovery is often manual and fragmented.

How to Claim Unclaimed Insurance Money

The claim process generally involves:

Step 1: Establish Policy Existence

Provide:

- Policy number (if available)

- Policyholder details

- Supporting evidence such as premium receipts

Step 2: Identity and Relationship Verification

Insurers require:

- Identity proof of claimant

- Proof of relationship (for nominees or heirs)

- Death certificate (in case of death claims)

Step 3: Claim Settlement

Once verified:

- Insurer releases the payable amount

- Interest may be added as per policy terms and regulatory norms

There is no expiry period for valid claims.

Claiming Insurance Money as a Legal Heir

If no nominee is registered, legal heirs may need:

- Legal heir certificate or succession certificate

- Indemnity bonds (in certain cases)

- Additional documentation for verification

Insurers follow strict due diligence to prevent wrongful claims.

Why Unclaimed Insurance Money Is Also a Data Problem

Unclaimed insurance funds highlight deeper systemic gaps:

- Fragmented identity data across insurers

- Outdated nominee and contact records

- Long policy tenures without periodic updates

- Poor linkage between identity, family, and financial records

Preventing unclaimed insurance is as much about data continuity as it is about claims processing.

The Role of Better Identity and Record Continuity

Regulators increasingly emphasize:

- Accurate customer identification

- Periodic KYC updates

- Clear nominee records

- Traceability across time

Strong digital identity infrastructure helps ensure that insurance benefits reach the right person at the right time.

The Hidden Identity Problems in Unclaimed Funds in India

Fragmented identity data in banking, insurance, and investment systems leads to mismatches that delay or prevent the recovery of unclaimed funds, highlighting the need for accurate identity verification.

The Hidden Identity Problems in Unclaimed Funds in India

Unclaimed funds in India whether in bank deposits, insurance policies, dividends, or retirement accounts are often treated as isolated financial lapses. In reality, they represent a systemic failure of identity continuity and data infrastructure.

These funds are not unclaimed because they are unknown. They are unclaimed because systems fail to reliably connect people, identities, and financial relationships over time.

Unclaimed Funds Are a Symptom, Not the Root Problem

Regulators have established clear custodial mechanisms for unclaimed funds through institutions such as the Reserve Bank of India, the Investor Education and Protection Fund, and the Insurance Regulatory and Development Authority of India.

Yet, despite regulatory safeguards, unclaimed balances continue to grow. This indicates that the issue is structural, not procedural.

At its core, unclaimed funds emerge when:

- Identity records fragment

- Ownership data becomes outdated

- Systems cannot reconcile past and present identities

Fragmented Identity Across Financial Institutions

Most individuals interact with multiple financial entities over their lifetime:

- Banks

- Insurance companies

- Employers

- Pension administrators

- Capital market intermediaries

Each institution maintains its own identity records often with no persistent linkage across time or across institutions.

As a result:

- A person becomes multiple identities in parallel systems

- Updates made in one institution are invisible to others

- Financial relationships decay silently into dormancy

Time Is the Biggest Enemy of Identity Systems

Unclaimed funds rarely arise quickly. They accumulate over years or decades.

Common triggers include:

- Change in address, phone number, or email

- Name changes due to marriage

- Job changes and employer transitions

- Migration across cities or countries

- Death without consolidated financial records

Legacy systems were never designed to maintain identity fidelity across long time horizons and unclaimed funds are the outcome.

Nominee Data: The Weakest Link

Nomination frameworks exist across banks, insurers, and pension systems, but nominee data is often:

- Missing

- Outdated

- Inconsistent across institutions

- Poorly communicated to families

When the primary account holder is no longer reachable, systems struggle to transition ownership smoothly causing funds to drift into custodial pools.

Data Silos Create Invisible Wealth

Each unclaimed fund pool whether under RBI, IEPF, or insurers operates independently.

This means:

- No unified view of an individual’s financial footprint

- No cross-institution discovery mechanism

- No automatic reconciliation of ownership across asset classes

For families, this creates a paradox: wealth exists, but visibility does not.

Why Compliance Alone Cannot Solve This

Regulatory compliance ensures:

- Funds are protected

- Claims are honoured

- Disclosure exists

But compliance does not ensure:

- Identity continuity

- Proactive discovery

- Cross-system reconciliation

Unclaimed funds are therefore not a compliance failure they are an infrastructure gap.

The Role of Digital Public Infrastructure

India’s push toward digital public infrastructure has shown that identity-linked systems reduce friction and increase accountability.

Effective infrastructure for preventing unclaimed funds must enable:

- Persistent identity resolution

- Entity and relationship mapping

- Data consistency across institutions

- Secure, privacy-aware reconciliation

This does not require centralization of data but interoperability of identity signals.

Why Institutions Need Better Identity Resolution

For banks, insurers, and financial platforms, unclaimed funds introduce:

- Long-term reconciliation liabilities

- Fraud risk in dormant accounts

- Operational and compliance overhead

- Poor customer and beneficiary experience

Stronger identity and data infrastructure reduces:

- Dormancy

- Ownership ambiguity

- Manual recovery processes

Unclaimed Funds as a Trust Signal

At a societal level, unclaimed funds erode trust:

- Individuals lose confidence in institutions

- Families struggle during financial distress

- Institutions carry reputational and operational burden

Solving unclaimed funds is therefore not just about recovery it is about trust continuity.

The Path Forward: From Custody to Continuity

Preventing future unclaimed funds requires a shift in thinking:

- From static KYC to continuous identity recognition

- From siloed records to linked relationships

- From reactive claims to proactive discovery

Identity, when treated as infrastructure rather than a one-time check, becomes the strongest defence against unclaimed wealth.

RBI Rules on Dormant Accounts

Dormant bank accounts arise when there are no customer-initiated transactions for two years. RBI rules define how such accounts are handled and how account holders can restore access.

RBI Rules on Dormant Accounts

Across India, a significant amount of money lies untouched in bank accounts not because it was forgotten forever, but because the account holders stopped operating them. These unclaimed bank deposits arise when savings accounts, current accounts, or fixed deposits remain inactive for extended periods.

To safeguard depositors’ interests and maintain transparency, the Reserve Bank of India (RBI) has laid down clear rules on how banks must classify, manage, and disclose such accounts while ensuring that depositors or their legal heirs can reclaim their money at any time.

What Are Unclaimed Bank Deposits?

Unclaimed bank deposits are balances in bank accounts that have seen no customer-initiated transactions for a continuous period of 10 years.

These deposits typically include:

- Savings and current account balances

- Fixed deposits that have matured but not been claimed

- Interest accrued on such deposits

Once this threshold is crossed, banks are required to transfer the funds to a central pool, while maintaining detailed records of the original owners.

Inactive vs Dormant Accounts: What’s the Difference?

RBI distinguishes between two stages of inactivity:

1. Inactive Account

An account is considered inactive if there are no customer-initiated transactions for 2 consecutive years.

2. Dormant Account

An account becomes dormant after 2 years of inactivity, triggering:

- Enhanced monitoring

- Restrictions to prevent misuse

- Mandatory customer re-verification before reactivation

Dormant accounts are closely tracked due to their higher vulnerability to fraud and misuse.

RBI Rules Governing Unclaimed Deposits

The RBI mandates banks to:

- Identify inactive and dormant accounts periodically

- Attempt to contact account holders using available details

- Publish details of unclaimed deposits on bank websites

- Transfer eligible deposits to the Depositor Education and Awareness Fund (DEAF) after 10 years

Despite the transfer, banks remain responsible for processing claims and returning funds to rightful owners.

What Is the Depositor Education and Awareness Fund (DEAF)?

The DEAF is a fund established under RBI directions to house unclaimed bank deposits.

Key points:

- Banks transfer eligible unclaimed balances to DEAF

- Funds remain claimable at all times

- Interest continues to accrue as per RBI guidelines

- Banks must honour valid claims even after transfer

The purpose of DEAF is custodianship not confiscation.

Why Do Bank Deposits Go Unclaimed?

Unclaimed deposits are often the result of long-term data and identity gaps, including:

- Change in address or contact information

- Death of account holder without nominee updates

- Multiple bank relationships across years

- Forgotten fixed deposits

- Poor awareness among legal heirs

In many cases, families are unaware that such accounts even exist.

How to Check for Unclaimed Bank Deposits

Individuals or heirs can check for unclaimed deposits by:

- Visiting bank websites that publish unclaimed deposit lists

- Using RBI-mandated centralized search facilities

- Contacting the branch where the account was held

Basic details such as name, last known address, and branch are usually sufficient to begin the search.

How to Claim Unclaimed Bank Deposits

The claim process generally involves:

Step 1: Submit a Claim Request

Approach the concerned bank branch with:

- Valid identity proof

- Account details (if available)

Step 2: Verification

Banks conduct:

- Identity verification

- KYC revalidation

- Legal heir verification (if applicable)

Step 3: Settlement

Once verified:

- Funds are released to the claimant

- Interest is paid as per applicable rules

There is no deadline for making a legitimate claim.

Claiming Unclaimed Deposits as a Legal Heir

Legal heirs may need to provide:

- Death certificate of the account holder

- Proof of relationship

- Succession certificate or legal heir certificate (in certain cases)

Banks follow due diligence to ensure funds reach the rightful claimant.

Why Dormant Accounts Pose a Risk for Banks

From a systemic perspective, dormant and unclaimed accounts increase:

- Fraud exposure

- Compliance burden

- Reconciliation challenges

- Identity mismatches across financial systems

This is why RBI places strong emphasis on continuous customer identification and record accuracy.

The Bigger Picture: Unclaimed Deposits as an Identity Challenge